Preamble

Investors who bought shares early in today’s China-tech-darlings have done well. If you were in the right stocks, at the right time, heavily weighted your portfolio in that direction and have taken no profits on the way up, you will now be, minted.

Congratulations to the lucky few described above. Most investors, however, were late to the party, hold a mixed bag of performers, and didn’t buy with the conviction necessary to propel them to stardom. Many have done OK but the legacy of missed opportunity means portfolios are now, in aggregate, overweight a sector that looks out of puff.

A Useful Lesson From Recent History

In 2007 China Mobile (CM) had revenue of Rmb357bn, it generated a net profit after tax (NPAT) of Rmb87bn from 369m subscribers and was believed to be capable of delivering high growth from that point. Expectations were, as its turned out, correct. By 2017 it’s revenue had grown to Rmb740bn and it was generating an NPAT of Rmb114bn from 887m subscribers. Over the ten-year period revenue rose by over 100%, NPAT by 31% and subscribers by 140%; and the share price? Down 30%*.

[*I’m using data here and for some examples below from Mr. David Webb’s excellent total return charts that correctly roll up dividends into long term reports. This is the only way to correctly analyze a stock over more than a couple of years. You can see the CM chart via this link Webb-Site CM Total Return]

Time And Again, And Again, And…

The example of CM highlights a mistake I see investors in China making over, and over again. Somehow the last generation of bilked hopefuls seems unable to pass on expensively acquired wisdom to the next. In my career I’ve seen this cycle play out in TVs, white-goods, telephony, autos, commodities, banks, and consumer plays (to name just a few!).

Some recent examples of one-time portfolio must-haves: China Minsheng Bank (#1988), Li and Fung (#494) and Parkson Retail (#3368). All were held out as outstanding prospects at various points in time and few institutional portfolios were absent these names in their high-flying stages. From their peaks they’re down 30%, 70% and 90% respectively.

Double Trouble

The fallen Angels highlighted above have, unlike CM, suffered a double-trouble. Not only have their valuations altered but their earnings have failed to grow as investors in happier times assumed they would. This can happen anywhere but in China, a market growing more rapidly than almost any other in the world, calamity is often accelerated. Department stores for example had their business models upended overnight by an e-commerce model that didn’t gradually emerge, it exploded.

The other problem that affects prospects in China and often suddenly hacks into profitability is competition. Credit for many has been priced around zero for a long time and businesses built on zero-cost finance can be very aggressive. There’s a battle going on at the moment in bike sharing that can only be understood if you imagine protagonists on all sides fighting with lots of no-cost cash. Investors must be aware in China a good idea and a head start are not the competitive advantages they often amount to in more developed markets.

Land Of Finite Promise

Chinazabigplace, we all know; but it’s not thaaat big.

This is another serial error investors in China make. In fact, as this slogan from 1850’s Britain illustrates, they’ve been making this mistake for a very long time; “[If we] could add an inch of material to every Chinaman’s shirt tail, the mills of Lancashire could be kept busy for a generation.” Need I point out the mills in Lancashire disappeared a long time ago? The error here is to believe because China is so darn big businesses are capable of near infinite growth.

Early investors in CM were reminded of this when they first started hearing the term ‘pre-paid customer’. In the early days of their growth the company was signing on mostly price-inelastic ‘contract’ customers with agreeably fat margins. As that rich seam became thinner, to maintain subscriber growth, the company shifted downmarket to more budget conscious customers which in large part explains why in the last ten years their revenue rose 100% but profit by only 30%.

Even in a market as big as China there are limits to how many pairs of shoes can be sold, how many will pay for the latest online gaming experience and how many luxury autos the market in a given year can absorb. More importantly, time and again, we see these limits being reached surprisingly quickly.

Do You See What I See?

According to a list compiled jointly by the Internet Society of China and the information center of Industry and Information Technology Ministry at the end of 2017 the top five internet companies in China were, in order, Tencent, Alibaba, Baidu, JD.com and NetEase.

Let’s look at the one-year charts (Yahoo Finance) for each:

Tencent

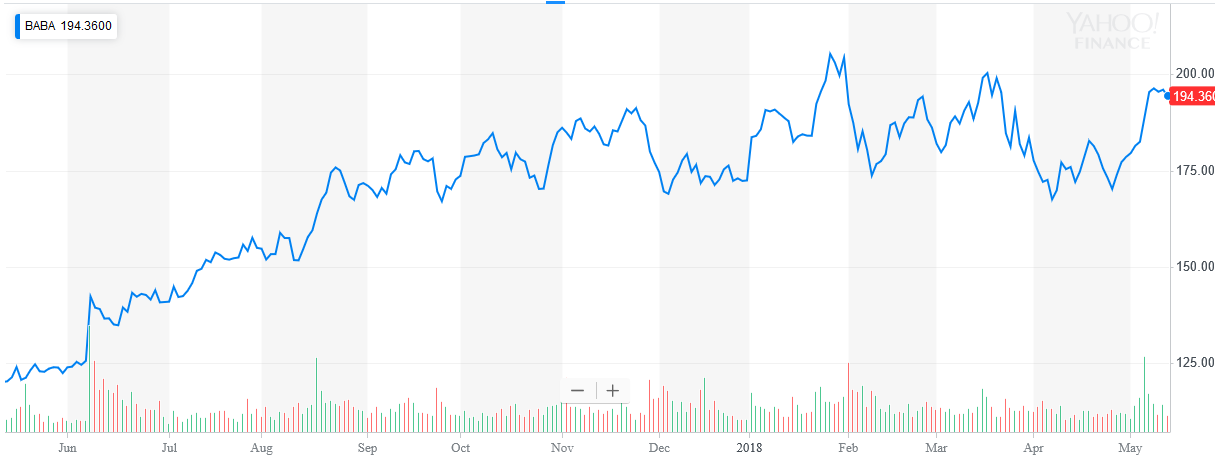

Alibaba

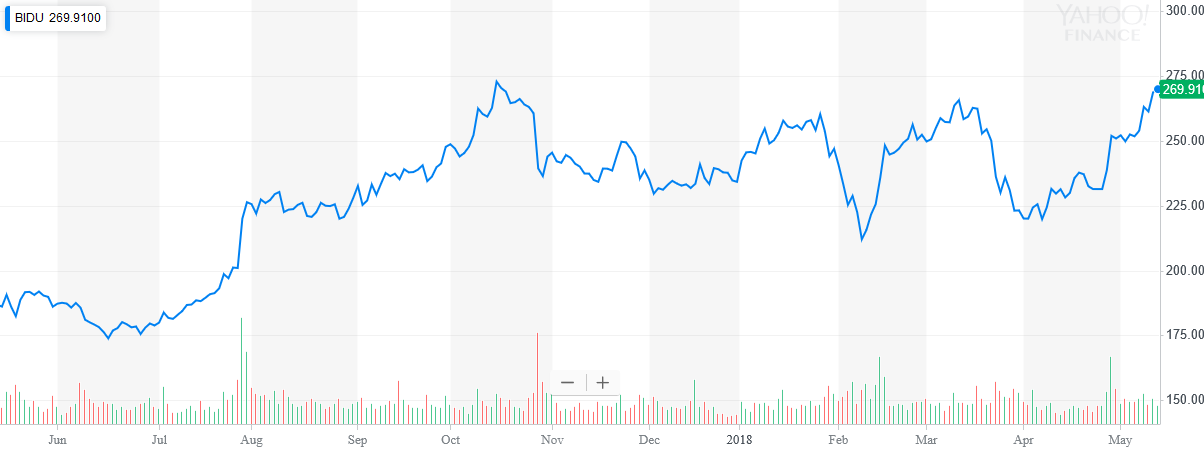

Baidu

Baidu

JD.com

JD.com

NetEase

NetEase

With the exception of Baidu (whose chart suggests imminent new highs) these charts look remarkably similar. We see a peak some time ago and then a long shuffle sideways.

With the exception of Baidu (whose chart suggests imminent new highs) these charts look remarkably similar. We see a peak some time ago and then a long shuffle sideways.

You’ll see the same picture for many others in the China-tech complex; and this is in the context of solid earnings growth for most.

Not Over Until It’s Over

To return to the question at the top of this note, has the bloom at last come of this rose?

Of course, I don’t know. The charts above may just be showing a much needed pause for breath before new summits are attempted. Or they show what happens inevitably to a go-go sector when expectations are beginning to mature.

The lesson from history is that whether a revaluation is taking place now or not is less important than to remember at some stage it, with sun-rising-in-the-east certainty, will.

Before We Go, A Little Math

A widely and often quoted China fund manager was reported on April 12th this year as saying she believed Tencent’s share price would exceed H$1,000 by 2020.

Last year the company managed earnings per share (EPS) of H$9.10 so, at Friday’s close of H$408.80, it’s historic price to earnings ratio (P/E) was 45x. Assuming the P/E remains the same for the next two years and is still at 45x on January 1st 2020, to support the H$1,000 target, it’s EPS will have to have risen by 140% (to H$22.10) or by 55% for each of the next two years.

In the last five years the company’s net profit grew by 22%, 54%, 21%, 43% and 74% respectively. Therefore, back to back growth of 55% this year and next isn’t impossible; but this is to overlook the likely prospect of the stock being valued somewhat lower than it’s present lofty 45x two years hence.

Assuming, more realistically, a valuation compression to, say 25x but leaving the high growth forecast intact where would the stock price be? H$550.00, [Bulls may insert ‘Ah-hah!’ here] or 35% higher than today’s price. A respectable proposition for sure; but a condition we have to go through very optimistic forecasting-hoops to arrive at.

In Conclusion

Is it over for China-tech?

No, China has produced some of the largest internet companies on the planet and these are not going away. Moreover, in coffee-shops and incubators all over the country, as I write, ideas are being refined by some of the finest minds in the world into business models that will amaze into the indefinite future.

What may be over though is the high price investors have been prepared to pay for the earnings of these companies, most especially the now well established operators.

Mobile telephony is more important than ever and China has never had more users on its system. China Mobile’s P/E however stands currently at a little over 11x; just saying..