That the multi-trillion dollar global institutional asset management business is built on various forms of the same incorrect theory is not something the industry likes to spend too much time thinking, or Heaven forbid, talking about; and it certainly has no interest in socializing this issue with its clients.

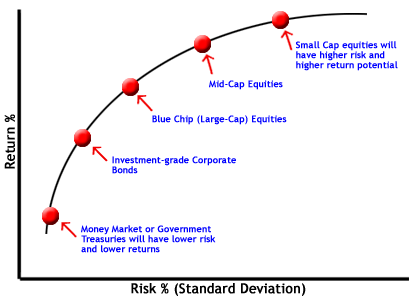

I’m referring specifically to the Capital Asset Pricing Model (CAPM). For non finance specialists a quick tutorial. Back in the 1950s Mr. Harry Markowitz developed a concept of risk along the highly intuitive lines that the more risk you take the higher rewards you should achieve. As not everyone likes risk he showed there’s a line (it’s not straight, which is important) from no-risk cash to the highest risk equities that you can draw based on return and then, depending on how much return you’re willing to trade for risk you can position yourself on this line accordingly. Moreover, in any market there’s a ‘beta’ return you get for just being there and an ‘alpha’ return you can get from picking higher risk winners. He got a Nobel Prize in 1990 for his work.

Just one teeny problem. The theory’s wrong.

The beautiful math that Markowitz’s theories spawned has been refined and used to build initially the mutual fund industry and latterly the hedge fund complex. Anyone who today uses the terms alpha or beta is implicitly supporting the CAPM misconception. Academics began to notice holes in the theory very early on and fans have been patching and repairing so it survives today, wheezing Cuban-clunker like, still performing the function it was originally designed for.

This week’s paper is dense but if you care about any of the above you should make the effort to read it in full (you can skip the math, it makes just as much sense and is far less frightening if you tune it out). In it Ashwin Alankar, Peter Blaustein and Myron S. Scholes a Senior Vice President with AllianceBernstein, an Oak Hill Advisors employee and the Frank E. Buck Professor of Finance, Emeritus, Stanford Graduate School of Business (and another Nobel Laureate, for a theory that really works) respectively tackle one of the most puzzling issues the CAPM says shouldn’t exist, what is called ‘the low volatility anomaly’.

First identified from US data it’s now been convincingly proved worldwide that (when adjusted for risk) portfolios of low risk assets consistently outperform portfolios of higher risk assets; the complete reverse of what the CAPM theory predicts. In investing at least the tortoise really does consistently beat the hare; but why should this be so?

Two theories have been most frequently referenced but this paper not only highlights their implausibility but instead advances and then proves another reason for the effect. [Sorry, this is a much longer summary than I usually end up writing but there’s a lot here!]. The first theory comes from behaviorists who suggest that markets attract gamblers who have a preference for high risk stocks so their prices are always artificially too high (which begets long term under-performance). Can’t be right say Myron et al. If it were, in times of high volatility these stocks would be extra popular and empirical evidence shows this is not the case. The second theory looks at manager constraints on leverage and suggests that leverage prohibition for many drives managers into riskier assets, which again bids their price asymmetrically up. Unlikely though, the researchers argue there’s enough managers with access to leverage to convincingly scuttle that argument.

The real problem, it seems, is the clients of institutional managers. Or, more specifically clients who give money to managers but insist on being able to get their money back quickly whilst the managers stick close to agreed benchmarks trying, at the client’s behest, to beat them. The agency issue of managers getting paid based on AUM and not their performance compounds the problem as few will dare to point out the irreconcilability of these conflicting constraints and the behavior that results.

Videlicet; in aggregate the world’s big money managers are always longer of higher risk assets than their benchmarks would imply. This is why the value of these assets is always too high leading to their long term under-performance. The need for liquidity means that even a manager attempting to replicate benchmark performance will have to compensate any cash holding with additional risk. Add to this the requirement to outperform, which can only come from more risky assets, and it’s now obvious where the over priced risky asset effect comes from.

The world of finance and economics is regularly observed to have this Schrödinger’s Cat like behavior and it’s ironic that Mr. Markowitz may have been more right than wrong in the 1950s but the wholesale adoption of his theory into practice by so many operators has guaranteed it’s error.

Especially for investors that operate a core-satellite approach a bit more core and a bit less satellite might therefore be in order? For managers who vex about beating benchmarks perhaps a more grown up discussion with clients may be due (hardly likely)?

The case for ETFs (not without their own systemic problems) appears to have never been stronger.

Happy Sunday!

[The full paper can be accessed via this link The Cost of Constraints]